2026 Tax Law Changes: New Deductions & Credits Guide

Anúncios

The upcoming 2026 tax law changes introduce significant shifts in deductions and credits, demanding proactive financial planning to optimize individual and business tax strategies.

Anúncios

Understanding the 2026 tax law changes is crucial for every American taxpayer and business owner. The landscape of deductions and credits is set for significant shifts, impacting everything from personal finances to corporate strategies. Are you prepared for what’s ahead?

Anúncios

Navigating the Sunset Provisions of the TCJA

The Tax Cuts and Jobs Act (TCJA) of 2017 brought about sweeping changes to the U.S. tax code, many of which are set to expire, or ‘sunset,’ at the end of 2025. This expiration will usher in a new era of tax regulations in 2026, reverting many provisions to their pre-TCJA state unless new legislation is enacted. This section delves into the primary sunset provisions and their anticipated impact.

The return to pre-TCJA tax brackets will likely be one of the most noticeable changes for individual taxpayers. While the TCJA generally lowered individual income tax rates, these are scheduled to increase across various income levels. Understanding your potential new bracket is the first step in preparing for these shifts.

Individual Income Tax Rate Adjustments

- Higher Tax Brackets: Expect a return to seven individual income tax brackets, with rates generally higher than those seen under the TCJA.

- Bracket Threshold Changes: The income thresholds for each bracket will adjust, potentially pushing more taxpayers into higher marginal rates.

- Impact on High Earners: High-income individuals may experience the most significant increases in their effective tax rates.

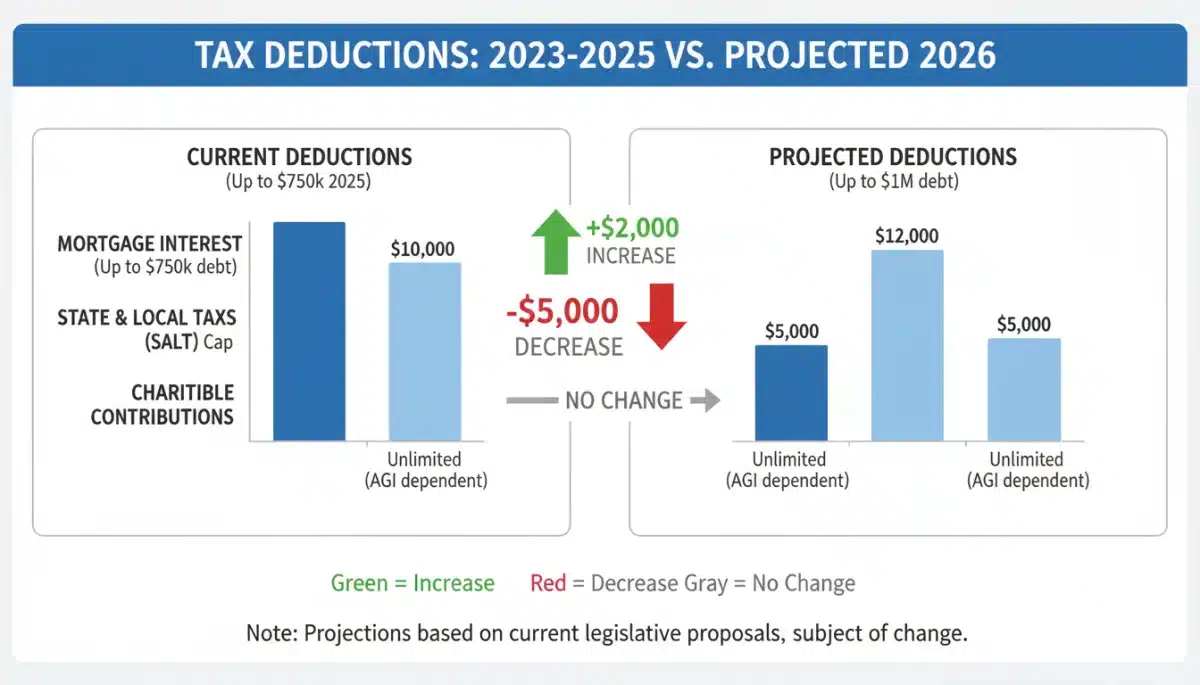

Beyond the tax rates themselves, several key deductions and credits are also on the chopping block or set for modification. The standard deduction, which was significantly increased under the TCJA, is projected to decrease, meaning fewer taxpayers might opt for the standard deduction and instead itemize.

In conclusion, the sunsetting of the TCJA provisions is not merely a technicality; it represents a fundamental recalibration of the tax burden on individuals and businesses. Proactive planning based on these impending changes is essential to mitigate potential negative impacts and identify new opportunities.

Anticipated Changes to Standard and Itemized Deductions

The interplay between standard and itemized deductions is a cornerstone of individual tax planning, and 2026 promises significant alterations in this area. The substantial increase in the standard deduction under the TCJA led many taxpayers to forgo itemizing. With the projected decrease of the standard deduction, a renewed focus on itemized deductions will become necessary for many households.

For those who previously found the increased standard deduction more advantageous, a smaller standard deduction might mean revisiting the benefits of itemizing. This could involve meticulous record-keeping for eligible expenses that were previously less impactful on tax outcomes.

Key Deduction Revisions to Watch

- Reduced Standard Deduction: The standard deduction amounts are expected to revert to pre-TCJA levels, adjusted for inflation. This change will likely compel more taxpayers to evaluate if itemizing is now more beneficial.

- State and Local Tax (SALT) Deduction Cap: The $10,000 cap on the SALT deduction, a contentious provision of the TCJA, is also set to expire. Its removal would allow taxpayers, particularly in high-tax states, to deduct the full amount of their state and local taxes, potentially leading to significant tax savings for some.

- Miscellaneous Itemized Deductions: The TCJA eliminated many miscellaneous itemized deductions subject to the 2% adjusted gross income (AGI) floor. These are not expected to return automatically.

Moreover, the personal exemption, which was effectively eliminated by the TCJA in favor of a higher standard deduction and an expanded child tax credit, is slated to return. This reintroduction could offer additional tax relief for larger families or those with dependents, but its exact value and interaction with other provisions remain to be seen.

Understanding these shifts in deductions is critical for optimizing your taxable income. Taxpayers should start reviewing their potential itemizable expenses now, including mortgage interest, charitable contributions, and medical expenses, to prepare for the 2026 tax year.

Updates to Key Tax Credits and Their Eligibility

Beyond deductions, tax credits play a vital role in reducing a taxpayer’s overall liability, offering a dollar-for-dollar reduction in taxes owed. The 2026 tax law changes are expected to bring modifications to several prominent credits, impacting families, students, and certain business activities. These changes could significantly alter the net tax burden for many.

The Child Tax Credit (CTC), a cornerstone for many families, saw temporary expansions during the pandemic that have since expired. While the TCJA increased the maximum CTC to $2,000 per child and made a portion refundable, this enhanced credit is also subject to the sunset provisions. Therefore, the credit amount and its refundability criteria are likely to revert.

Anticipated Credit Modifications

- Child Tax Credit (CTC): The CTC is expected to revert to its pre-TCJA structure, potentially reducing the maximum credit amount and altering income phase-out thresholds. This could mean a smaller credit for many families.

- Education Credits: While various education credits exist, their income limitations and eligibility requirements are frequently reviewed. Any changes here could affect how much students and their families can claim for higher education expenses.

- Energy-Efficient Home Credits: The push for green initiatives often includes tax incentives. While some credits are more permanent, others are temporary or subject to renewal. Taxpayers investing in energy-efficient home improvements should monitor developments in this area.

The Earned Income Tax Credit (EITC), designed to benefit low-to-moderate income working individuals and families, is generally a more stable credit. However, even credits like the EITC can undergo adjustments to income thresholds or maximum credit amounts. Monitoring these potential changes is essential for eligible taxpayers to ensure they claim the full benefit they are entitled to.

In summary, staying informed about the specifics of tax credit changes is paramount. These credits can offer substantial relief, and even small adjustments to eligibility or amounts can have a considerable impact on a household’s financial well-being. Proactive research and consultation with a tax professional can help ensure you maximize any available credits in 2026.

Business Tax Implications and Corporate Rate Adjustments

While much of the public discourse around 2026 tax law changes focuses on individual taxpayers, businesses, from small enterprises to large corporations, will also face significant adjustments. The corporate tax rate, which was drastically reduced by the TCJA, is a primary area of potential revision. These changes can directly impact profitability, investment decisions, and overall economic strategy.

The corporate tax rate was slashed from a high of 35% to a flat 21% under the TCJA. This reduction was a major incentive for businesses to invest and expand within the U.S. Should this rate increase, companies will need to re-evaluate their financial models and potentially adjust their pricing, hiring, or expansion plans.

Key Business Tax Considerations

- Corporate Income Tax Rate: There is a strong possibility of an increase in the corporate income tax rate, potentially moving closer to pre-TCJA levels or a modified rate that aims to balance revenue generation with business competitiveness.

- Qualified Business Income (QBI) Deduction: The Section 199A deduction for qualified business income, which allows eligible pass-through entities to deduct up to 20% of their qualified business income, is also set to expire. Its expiration would significantly impact sole proprietors, partnerships, and S corporations.

- Depreciation Rules: Certain enhanced depreciation provisions, such as 100% bonus depreciation, are also phasing out. Businesses relying on accelerated depreciation for capital expenditures will need to factor in reduced deductions for new assets.

Small businesses, in particular, may feel the brunt of changes to the QBI deduction and other pass-through entity provisions. Many small businesses are structured as pass-through entities, meaning their profits are taxed at the owner’s individual income tax rate. The loss of the QBI deduction could lead to a substantial increase in their tax liability.

Ultimately, businesses must engage in thorough financial forecasting and scenario planning to account for these potential tax shifts. Understanding how these changes will affect cash flow, investment returns, and competitive positioning is vital for sustained success in the evolving tax environment.

Strategies for Proactive Tax Planning in 2026

Given the anticipated 2026 tax law changes, a reactive approach to tax planning will be insufficient. Proactive strategies are essential for individuals and businesses to navigate the evolving tax landscape effectively, minimize liabilities, and maximize financial opportunities. Starting early allows for thoughtful adjustments to financial behaviors and investment decisions.

One of the most immediate steps is to consult with a qualified tax professional. A knowledgeable advisor can provide personalized guidance based on your specific financial situation, helping you understand how the proposed changes will impact you directly and offering tailored strategies for mitigation and optimization.

Essential Planning Steps

- Review Current Financial Situation: Conduct a comprehensive review of your income, deductions, and credits from recent tax years to establish a baseline. This will help identify areas most susceptible to change.

- Project Future Income and Expenses: Forecast your expected income, significant expenses, and potential life events (e.g., marriage, birth of a child, retirement) for 2026 to anticipate their tax implications.

- Optimize Investment Strategies: Consider the tax implications of your investment portfolio. This might involve rebalancing, tax-loss harvesting, or adjusting contributions to tax-advantaged accounts like 401(k)s and IRAs, especially if tax rates are expected to rise.

For individuals, re-evaluating withholding or estimated tax payments is crucial to avoid underpayment penalties. If your tax liability is projected to increase, adjusting these payments throughout 2026 can help manage cash flow and prevent a large tax bill at year-end. Businesses should also review their quarterly estimated tax payments.

Furthermore, consider accelerating income or deferring deductions where strategically advantageous before the end of 2025, if specific provisions are set to expire or become less favorable. Conversely, deferring income or accelerating deductions might be beneficial if future tax rates are expected to be lower, though this is less likely given the current outlook.

In conclusion, proactive tax planning is not about avoiding taxes, but about optimizing your financial position within the legal framework. By staying informed, consulting experts, and making timely adjustments, you can navigate the 2026 tax changes with confidence and secure your financial future.

The Broader Economic Impact of 2026 Tax Reforms

The 2026 tax law changes extend far beyond individual tax returns and corporate balance sheets. These reforms are poised to have a significant ripple effect across the broader U.S. economy, influencing everything from consumer spending and investment to inflation and international competitiveness. Understanding these macroeconomic implications is crucial for both policymakers and citizens.

One primary area of impact is consumer behavior. If individual income tax rates rise and certain deductions become less generous, households may experience a decrease in disposable income. This could lead to a reduction in consumer spending, which is a major driver of economic growth. Businesses, in turn, might face reduced demand for their products and services.

Economic Considerations

- Consumer Spending: A potential decrease in disposable income due to higher taxes could dampen consumer spending, impacting retail and service sectors.

- Investment and Capital Formation: Changes to corporate tax rates and business deductions could influence corporate investment decisions, potentially affecting capital formation and job creation.

- Inflationary Pressures: While not a direct consequence, tax policy can interact with monetary policy to exacerbate or mitigate inflationary pressures, depending on how changes affect aggregate demand.

Moreover, the international competitiveness of U.S. businesses could be affected if the corporate tax rate increases significantly. A higher domestic tax burden might make the U.S. less attractive for foreign investment and could encourage American companies to seek more favorable tax environments abroad, potentially leading to job losses domestically.

The impact on government revenue is another critical aspect. The sunsetting provisions are expected to increase federal tax receipts, which could help address the national debt or fund new government programs. However, the exact revenue impact will depend on the final legislative package, if any, that replaces or modifies the expiring provisions.

In essence, the 2026 tax reforms are not just about numbers on a form; they represent a significant economic lever. Their ultimate design and implementation will play a crucial role in shaping the U.S. economic trajectory for years to come, affecting everything from individual prosperity to national economic stability.

Preparing for Enforcement and Compliance in 2026

As the 2026 tax law changes loom, taxpayers and businesses must not only understand the new rules but also prepare for potential shifts in enforcement and compliance. The Internal Revenue Service (IRS) will be tasked with implementing these new regulations, and its capacity and focus could impact how taxpayers experience the transition. Enhanced compliance measures or increased audit activity could be part of the new landscape.

The IRS has faced challenges with staffing and resources in recent years. However, with new funding initiatives, there’s an expectation of increased capacity. This could translate into more robust enforcement of tax laws, including those newly enacted or reinstated in 2026. Therefore, accurate record-keeping and a thorough understanding of obligations will be more critical than ever.

Compliance Best Practices

- Maintain Meticulous Records: Keep detailed records of all income, expenses, and transactions that could affect your tax liability. This includes digital and physical documentation.

- Stay Updated on IRS Guidance: Regularly check official IRS publications, notices, and FAQs as they release guidance on the new tax laws. Relying on unofficial sources can lead to errors.

- Leverage Professional Expertise: Engage with tax professionals who are knowledgeable about the latest changes. Their expertise can help ensure accurate filing and compliance, reducing the risk of penalties.

Furthermore, with changes in deductions and credits, taxpayers may find the complexity of their tax returns increasing. This might necessitate a greater reliance on tax preparation software or professional services. Understanding the nuances of new eligibility criteria for credits and the revised limitations on deductions will be key to avoiding common compliance pitfalls.

The emphasis on digital transactions and reporting continues to grow. Taxpayers should ensure their digital records are secure, accessible, and compliant with any new electronic filing requirements. Cybersecurity best practices are also paramount to protect sensitive financial information.

In conclusion, preparing for 2026 means more than just knowing the new tax rates; it involves adopting a disciplined approach to record-keeping, staying informed through official channels, and seeking expert advice when needed. A proactive stance on compliance will minimize stress and help ensure a smooth transition into the new tax year.

| Key Change Area | Brief Description of Impact |

|---|---|

| Individual Tax Rates | Reversion to higher, pre-TCJA income tax brackets for individuals. |

| Standard Deduction | Projected decrease, potentially encouraging more itemizing. |

| Child Tax Credit | Expected reversion to pre-TCJA amounts and eligibility rules. |

| Corporate Tax Rate | Potential increase from the current 21% flat rate. |

Frequently Asked Questions About 2026 Tax Changes

The main drivers are the sunset provisions of the Tax Cuts and Jobs Act (TCJA) of 2017, which means many temporary tax breaks for individuals are set to expire. Unless new legislation is passed, tax rates, deductions, and credits will revert to their pre-TCJA forms, adjusted for inflation.

The standard deduction is expected to decrease significantly, reverting to its pre-TCJA levels, adjusted for inflation. This change will likely lead more taxpayers to consider itemizing deductions if their qualifying expenses exceed the new, lower standard deduction amount.

Yes, the Child Tax Credit (CTC) is projected to revert to its pre-TCJA structure. This means the maximum credit amount may decrease, and the income phase-out thresholds and refundability rules could change, impacting the benefit for many families.

Businesses should anticipate potential increases in the corporate income tax rate and the expiration of the Qualified Business Income (QBI) deduction (Section 199A). Enhanced depreciation rules are also phasing out, impacting capital expenditure planning for many companies.

Start by reviewing your current financial situation, projecting future income, and consulting with a tax professional. Consider optimizing investment strategies and adjusting tax withholdings or estimated payments. Proactive planning is key to mitigating potential impacts and identifying new opportunities.

Conclusion

The impending 2026 tax law changes represent a pivotal moment for financial planning in the United States. With numerous provisions from the Tax Cuts and Jobs Act of 2017 set to expire, individuals and businesses alike must prepare for significant shifts in income tax rates, standard and itemized deductions, and various tax credits. The transition demands a proactive, informed approach, emphasizing meticulous record-keeping, continuous monitoring of official IRS guidance, and strategic consultation with tax professionals. By understanding these complex changes and their broader economic implications, taxpayers can navigate the evolving landscape effectively, ensuring compliance and optimizing their financial outcomes in the years to come. Staying ahead of these reforms is not just a recommendation, but a necessity for financial resilience and growth.