Strategic Budgeting 2026: 3-Month Plan to Cut Spending

Anúncios

A 3-month strategic budgeting plan for 2026 offers practical solutions to systematically identify and eliminate unnecessary spending, fostering greater financial stability and allowing for smarter money decisions.

Anúncios

Embarking on a journey towards financial mastery requires more than just good intentions; it demands a clear roadmap. This article provides a comprehensive guide to strategic budgeting 2026, outlining a practical 3-month plan designed to pinpoint and eliminate unnecessary expenditures, ultimately empowering you to take firm control of your financial future.

Anúncios

Understanding the Need for Strategic Budgeting

In today’s dynamic economic landscape, merely tracking expenses is often not enough to achieve significant financial goals. Strategic budgeting goes beyond simple categorization; it involves a proactive analysis of spending habits, aligning them with long-term objectives, and making informed decisions to optimize resource allocation. The year 2026 presents unique opportunities and challenges, making a strategic approach more crucial than ever for both individuals and households.

Many individuals find themselves caught in a cycle of reactive spending, addressing financial needs as they arise rather than anticipating them. This often leads to unnecessary expenses accumulating, hindering savings, and delaying important investments. A strategic budget acts as a compass, guiding financial decisions with purpose and foresight, ensuring every dollar works towards your financial well-being.

The pitfalls of reactive spending

Reactive spending, characterized by impulsive purchases and a lack of foresight, can erode financial stability over time. It often stems from a lack of awareness regarding where money truly goes, leading to a disconnect between income and actual financial outcomes. Identifying these reactive patterns is the first step toward building a more robust financial framework.

- Unplanned purchases due to promotions or social pressure.

- Overspending on non-essential services without regular review.

- Ignoring small, recurring subscriptions that add up significantly.

- Lack of emergency fund, leading to debt for unexpected costs.

The core of strategic budgeting lies in transforming these reactive habits into deliberate choices. By understanding the ‘why’ behind each expenditure, you can begin to differentiate between needs and wants, paving the way for more intentional financial behavior. This foundational understanding is essential before diving into the detailed 3-month plan.

Month 1: The Discovery Phase – Uncovering Spending Patterns

The first month of our strategic budgeting 2026 plan is dedicated to a deep dive into your current financial situation. This is not about judgment, but about honest observation. You cannot effectively eliminate unnecessary spending until you truly understand where your money is going. This phase requires meticulous tracking and categorization of every single expense, no matter how small.

Begin by gathering all your financial statements: bank accounts, credit cards, and any other payment platforms. The goal is to create a comprehensive snapshot of your financial inflows and outflows. Digital tools and apps can significantly simplify this process, providing automated categorization and visual representations of your spending.

Detailed expense tracking techniques

Effective expense tracking is the bedrock of any successful budget. This month, commit to recording every transaction. Whether you use a spreadsheet, a budgeting app, or a simple notebook, consistency is key. Focus on granularity; instead of just ‘groceries,’ try to break it down into ‘staples,’ ‘snacks,’ and ‘dining out.’

- Utilize budgeting apps like Mint, YNAB, or Personal Capital for automated tracking.

- Manually review bank and credit card statements weekly to catch discrepancies.

- Categorize every expense into clear, predefined groups (e.g., housing, transportation, food, entertainment).

- Keep a daily spending diary for one week to capture small, forgotten cash transactions.

Once you have a month’s worth of data, sit down and analyze it. Look for patterns, recurring expenses, and areas where your spending deviates from what you perceived. This objective data will illuminate potential areas for adjustment in the subsequent months. The discovery phase is crucial for building awareness and setting realistic goals for eliminating unnecessary spending.

Month 2: The Analysis Phase – Identifying Unnecessary Spending

With a full month of detailed spending data from the discovery phase, month two shifts to critical analysis. This is where you actively identify and challenge every single expenditure, asking yourself if it truly aligns with your financial goals and values. This phase is about making tough choices and distinguishing between essential needs and discretionary wants that may no longer serve you.

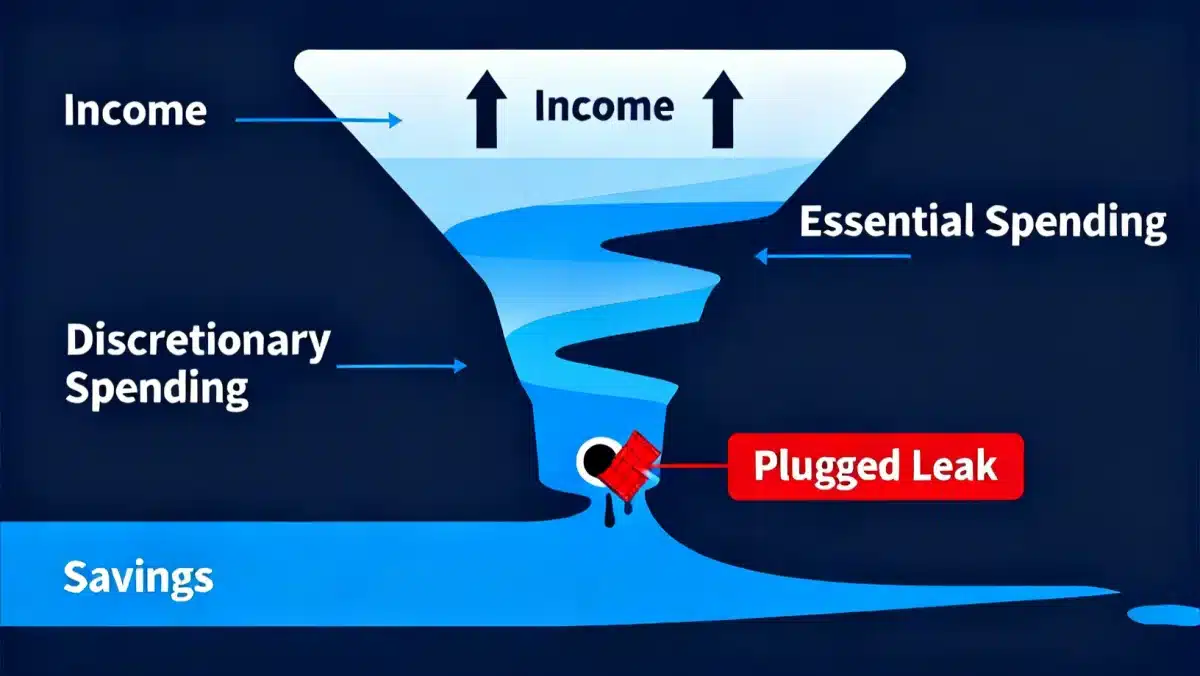

Review each category of spending. Highlight items that appear to be ‘leaks’ – expenses that provide little value or could be significantly reduced without impacting your quality of life. Be honest with yourself about what constitutes ‘unnecessary.’ This might include unused subscriptions, excessive dining out, or impulse purchases that bring fleeting satisfaction.

Categorizing and challenging expenses

Create two main categories: ‘Essential’ and ‘Non-Essential.’ Within ‘Non-Essential,’ identify a sub-category for ‘Unnecessary.’ This structured approach helps in making informed decisions. For each ‘Unnecessary’ item, consider alternatives or complete elimination. This involves more than just cutting; it’s about re-evaluating priorities.

- List all recurring subscriptions and cancel those that are no longer used or valued.

- Analyze entertainment spending and identify cheaper or free alternatives.

- Review grocery bills for impulse buys and plan meals more strategically.

- Evaluate transportation costs, exploring carpooling, public transport, or walking options.

This month requires a proactive mindset. Don’t just identify the leaks; actively brainstorm solutions to plug them. Engage in discussions with family members if it’s a household budget, ensuring everyone is on board with the changes. The goal is to move from passive observation to active decision-making, setting the stage for actionable reductions.

Month 3: The Implementation Phase – Eliminating and Optimizing

Having identified your unnecessary spending in month two, month three is all about taking concrete action. This is the implementation phase where you put your plans into motion, eliminating identified waste and optimizing your remaining expenditures. This month is about building new, healthier financial habits that will sustain your budget long-term.

Start by canceling those unused subscriptions and negotiating better rates for services you genuinely need, such as internet or insurance. Implement the alternative strategies you brainstormed, whether it’s cooking more at home, opting for free entertainment, or reducing impulse shopping. Small, consistent actions will yield significant results over time.

Strategies for sustainable spending reduction

Eliminating unnecessary spending isn’t a one-time event; it’s an ongoing process. Focus on creating sustainable habits that prevent unnecessary expenses from creeping back into your budget. This involves setting up automated transfers to savings, creating weekly spending limits for discretionary categories, and regularly reviewing your budget to ensure it remains aligned with your goals.

- Automate savings transfers to prevent discretionary spending from consuming savings.

- Set strict weekly or monthly limits for categories like dining out or entertainment.

- Unsubscribe from promotional emails that encourage impulse purchases.

- Implement a ‘cooling-off period’ for non-essential purchases (e.g., wait 48 hours before buying).

Beyond cutting, this phase also involves optimizing. Can you get more value for your essential spending? Perhaps switching to a different grocery store or finding a more fuel-efficient commute. The goal is to maximize the utility of every dollar, ensuring your budget is not just lean, but also smart and efficient. This month solidifies the changes and prepares you for ongoing financial management in 2026.

Practical Solutions for Common Spending Traps in 2026

Even with a well-structured plan, certain spending traps can derail your efforts. In 2026, with evolving technologies and consumer habits, these traps can be particularly insidious. This section explores common areas where unnecessary spending often occurs and provides practical, actionable solutions to navigate them effectively, ensuring your strategic budgeting 2026 remains on track.

One major trap is the ‘convenience tax’ – paying extra for things that save you time but drain your wallet. This includes excessive food delivery, pre-packaged meals, and premium services that offer marginal benefits. Another is the ‘keeping up with the Joneses’ syndrome, where social pressure leads to spending beyond your means on non-essential items.

Addressing digital subscription overload

The proliferation of streaming services, apps, and online memberships can quickly lead to subscription fatigue and significant recurring costs. Many subscriptions go unused or are forgotten, yet continue to auto-renew. Regularly auditing these digital commitments is paramount to preventing financial leaks.

- Create a master list of all digital subscriptions, including renewal dates and costs.

- Set calendar reminders for renewal dates to review usage before automatic charges.

- Consider bundle deals for streaming services or rotate subscriptions throughout the year.

- Explore free alternatives for productivity tools or entertainment where possible.

Another area to scrutinize is food spending. While essential, it’s also one of the easiest categories to overspend in. Meal planning, batch cooking, and bringing lunch from home can drastically reduce costs associated with dining out and impulse grocery purchases. By proactively addressing these common traps, you can reinforce your budgeting efforts and achieve greater financial resilience in 2026.

Maintaining Your Strategic Budget Beyond 3 Months

Completing the initial 3-month strategic budgeting plan is a significant achievement, but the journey doesn’t end there. True financial mastery comes from consistent application and periodic review. Your financial life is not static, and neither should your budget be. As income, expenses, and goals evolve, your budget must adapt accordingly. This ongoing process ensures that your strategic budgeting 2026 remains effective for the long haul.

Regular check-ins are vital. Schedule a dedicated time each month to review your spending, assess your progress towards goals, and make any necessary adjustments. This could be a weekly quick glance or a more thorough monthly reconciliation. The key is to stay engaged with your financial data and prevent old habits from creeping back in.

Establishing long-term financial habits

Beyond the numbers, strategic budgeting is about cultivating a healthier relationship with money. This involves developing habits that promote thoughtful spending and consistent saving. These habits, once ingrained, become second nature, making financial management less of a chore and more of an empowering routine.

- Implement a ‘zero-based budget’ periodically to ensure every dollar has a purpose.

- Set up automated transfers to savings and investment accounts immediately after payday.

- Regularly educate yourself on personal finance topics and economic trends.

- Celebrate small financial wins to reinforce positive budgeting behaviors.

Furthermore, consider setting up a financial buffer or ‘slush fund’ for unexpected, but not catastrophic, expenses. This helps prevent minor emergencies from derailing your carefully crafted budget. By embracing these long-term strategies, you can ensure that the initial three months of focused effort translate into lasting financial security and growth throughout 2026 and beyond.

| Key Phase | Description and Goal |

|---|---|

| Month 1: Discovery | Track all expenses meticulously to understand current spending habits. |

| Month 2: Analysis | Identify and categorize unnecessary spending based on collected data. |

| Month 3: Implementation | Actively eliminate identified waste and optimize remaining expenses. |

| Beyond 3 Months | Maintain, review, and adapt the budget for ongoing financial health. |

Frequently asked questions about strategic budgeting

Strategic budgeting in 2026 involves a proactive, forward-looking approach to managing finances. It focuses on aligning spending with long-term financial goals, identifying and eliminating waste, and adapting to economic changes, rather than just basic expense tracking.

Begin by meticulously tracking all expenses for a month. Then, categorize them as essential or non-essential. Critically evaluate non-essential items, asking if they provide real value or if alternatives exist. Look for recurring, unused subscriptions or impulse purchases.

Several tools can assist, including budgeting apps like Mint, YNAB (You Need A Budget), or Personal Capital. Spreadsheets (Excel, Google Sheets) are also effective for manual tracking. Choose a tool that fits your comfort level and provides clear categorization.

Absolutely. Maintaining a strategic budget long-term requires consistent review and adaptation. Schedule monthly check-ins, automate savings, and be flexible to adjust as your financial situation or goals change. It’s an ongoing process of refinement.

To avoid spending traps, be aware of impulse triggers, regularly audit subscriptions, and challenge the ‘convenience tax.’ Implement a waiting period for non-essential purchases and focus on value over immediate gratification to make more conscious spending decisions.

Conclusion

Embracing a strategic budgeting 2026 plan is more than just cutting costs; it’s about making deliberate choices that lead to lasting financial well-being. By dedicating three months to discovery, analysis, and implementation, you can systematically identify and eliminate unnecessary spending, transforming your financial habits and securing a more stable future. This proactive approach empowers you to navigate the complexities of modern finances with confidence, ensuring every dollar aligns with your personal and household goals for years to come.