U.S. Capital Gains Tax 2026: Portfolio Management

Anúncios

Understanding U.S. Capital Gains Tax in 2026 is essential for investors seeking to optimize their portfolios, requiring a clear grasp of tax rates and strategic planning.

Navigating the complexities of investment returns and taxation can be a daunting task for many, but a clear understanding of the tax landscape is paramount for financial success. For investors in the United States, comprehending U.S. Capital Gains Tax in 2026: Strategies for Efficient Portfolio Management is not just beneficial, but absolutely critical for optimizing returns and minimizing liabilities. This guide aims to demystify these regulations, offering insights and actionable strategies to help you manage your investments wisely as we look towards 2026 and beyond.

Anúncios

The Fundamentals of Capital Gains Tax in 2026

Capital gains tax is levied on the profit realized from the sale of a non-inventory asset that was purchased at a lower price. This includes assets like stocks, bonds, real estate, and even collectibles. Understanding the fundamental categories of capital gains—short-term and long-term—is the first step toward effective tax planning.

Anúncios

Short-term capital gains are profits from assets held for one year or less. These gains are typically taxed at your ordinary income tax rate, which can be significantly higher than long-term rates. Long-term capital gains, on the other hand, are profits from assets held for more than one year. These enjoy preferential tax rates, making the holding period a critical factor in investment decisions.

Distinguishing Short-Term vs. Long-Term Gains

The distinction between short-term and long-term capital gains hinges entirely on the holding period of the asset. This seemingly simple rule has profound implications for your tax bill. Investors often overlook the critical one-year mark, inadvertently triggering higher tax rates on what could have been a more tax-efficient transaction.

- Short-Term Gains: Assets held for 365 days or less.

- Long-Term Gains: Assets held for 366 days or more.

- Tax Rate Impact: Short-term gains are taxed as ordinary income; long-term gains have lower, preferential rates.

- Strategic Holding: Deliberately holding assets longer can significantly reduce tax liability.

The tax implications of this distinction underscore the importance of patient investing. Rash decisions to sell an asset just before the one-year mark can lead to a substantial increase in your tax burden, directly impacting your net returns. Therefore, strategic timing of sales is a cornerstone of efficient portfolio management.

In summary, a clear grasp of the difference between short-term and long-term capital gains is foundational. It empowers investors to make informed decisions that align with their financial goals while optimizing their tax position, setting the stage for more advanced strategies.

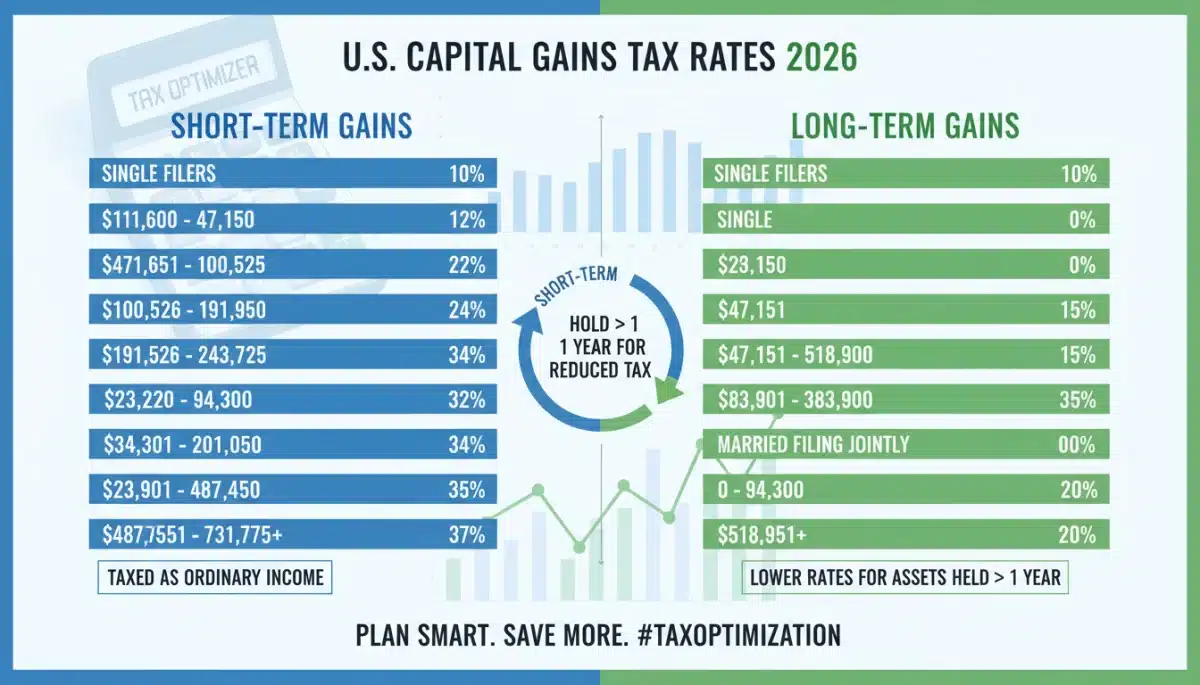

Anticipated Capital Gains Tax Rates for 2026

While specific tax legislation can evolve, we can project the likely framework for U.S. capital gains tax rates in 2026 based on current laws and anticipated economic trends. The rates for long-term capital gains are typically 0%, 15%, or 20%, depending on your taxable income. Short-term capital gains, as mentioned, are taxed at ordinary income rates, which could range from 10% to 37% or higher.

It’s crucial to understand how your overall income bracket influences these rates. For instance, individuals in lower income brackets might qualify for the 0% long-term capital gains rate, offering a significant advantage. As income rises, so does the long-term capital gains tax rate, reaching 15% and then 20% for high-income earners.

Income Thresholds and Rate Brackets

The income thresholds for each capital gains tax bracket are adjusted annually for inflation. For 2026, these thresholds are expected to reflect these adjustments, meaning investors need to stay updated on the exact figures to accurately plan. These brackets are critical because they determine which rate applies to your long-term gains, directly affecting your after-tax returns.

- 0% Rate: Typically for lower income individuals and couples.

- 15% Rate: Applies to the majority of middle to upper-middle-income taxpayers.

- 20% Rate: Reserved for high-income earners.

- Net Investment Income Tax (NIIT): An additional 3.8% tax for high-income individuals on certain investment income.

Beyond the standard rates, high-income earners must also consider the Net Investment Income Tax (NIIT), a 3.8% surcharge on certain investment income, including capital gains, for those exceeding specific adjusted gross income (AGI) thresholds. This additional tax further elevates the importance of strategic planning for affluent investors.

Staying informed about these anticipated rates and income thresholds is vital for anyone engaged in investment activities. Proactive planning based on these projections allows investors to make timely adjustments to their portfolios, ensuring they remain tax-efficient and aligned with their financial objectives.

Strategic Portfolio Management for Tax Efficiency

Effective portfolio management extends beyond simply choosing the right investments; it also involves optimizing those investments for tax efficiency. This means employing strategies that minimize your tax liabilities while maximizing your after-tax returns. Several powerful techniques can be integrated into your investment approach to achieve this.

One primary strategy is tax-loss harvesting, which involves selling investments at a loss to offset capital gains and, potentially, a limited amount of ordinary income. Another crucial strategy is the strategic use of tax-advantaged accounts, such as 401(k)s, IRAs, and HSAs, which offer various tax benefits that can significantly reduce your overall tax burden.

Utilizing Tax-Loss Harvesting Effectively

Tax-loss harvesting is a proactive strategy where you sell investments that have declined in value to realize a capital loss. These losses can then be used to offset any capital gains you might have, reducing your taxable income. If your capital losses exceed your capital gains, you can deduct up to $3,000 of the remaining loss against your ordinary income each year, carrying forward any excess losses to future years.

To implement tax-loss harvesting successfully, it’s essential to be aware of the wash-sale rule. This rule prevents you from claiming a loss on a security if you buy the same or a “substantially identical” security within 30 days before or after the sale. Careful timing and selection of replacement investments are key to avoiding this pitfall.

By regularly reviewing your portfolio for potential tax-loss harvesting opportunities, especially towards the end of the year, you can significantly enhance your overall tax efficiency. This strategy not only reduces your current tax bill but also provides flexibility for future tax planning.

Leveraging Tax-Advantaged Accounts

Tax-advantaged accounts are powerful tools for efficient portfolio management, offering benefits such as tax-deferred growth or tax-free withdrawals. Understanding the nuances of each account type and how they can be integrated into your financial plan is crucial for maximizing their potential. These accounts are not just for retirement; some offer benefits for healthcare and education, providing broad utility.

For instance, traditional 401(k)s and IRAs allow pre-tax contributions, meaning your taxable income is reduced in the year of contribution, and your investments grow tax-deferred until retirement. Roth 401(k)s and IRAs, conversely, involve after-tax contributions but offer tax-free withdrawals in retirement, making them highly attractive for those who expect to be in a higher tax bracket later in life.

Exploring Different Account Types

Each tax-advantaged account serves a specific purpose and comes with its own set of rules and benefits. A diversified approach often involves utilizing a combination of these accounts to meet various financial goals while optimizing tax outcomes. The choice depends heavily on your current income, future income expectations, and financial objectives.

- 401(k) and IRA (Traditional vs. Roth): Excellent for retirement savings with differing tax benefits.

- Health Savings Accounts (HSAs): Triple tax advantage for healthcare expenses.

- 529 Plans: Tax-advantaged savings for education expenses.

- Annuities: Offer tax-deferred growth, often used for retirement income.

HSAs are particularly noteworthy for their “triple tax advantage”: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. For those with high-deductible health plans, an HSA can be an invaluable tool for both healthcare savings and investment. Similarly, 529 plans provide tax-free growth and withdrawals for qualified education expenses, making them ideal for saving for college.

Integrating these tax-advantaged accounts into your portfolio strategy requires careful consideration of your personal financial situation and goals. By doing so, you can significantly reduce your tax burden over the long term and enhance your overall financial security.

Estate Planning and Capital Gains

Estate planning is an often-overlooked aspect of efficient portfolio management, particularly concerning capital gains. The way assets are structured and passed down can have significant tax implications for heirs. Understanding the “step-up in basis” rule and other estate planning tools is crucial for minimizing capital gains tax for your beneficiaries.

The step-up in basis rule is a significant advantage for heirs. When an inherited asset is sold, its cost basis is “stepped up” to its fair market value on the date of the original owner’s death. This means that any appreciation in value that occurred during the original owner’s lifetime is not subject to capital gains tax for the heir, potentially saving them a substantial amount.

The Step-Up in Basis Rule Explained

The step-up in basis rule is one of the most powerful tax benefits in estate planning. It effectively erases the capital gains that would have been realized if the asset had been sold by the original owner before their death. This can lead to considerable tax savings for beneficiaries, especially for assets that have appreciated significantly over a long period.

- Inherited Assets: Basis adjusted to market value at death.

- Eliminates Lifetime Gains: Heirs avoid capital gains tax on prior appreciation.

- Planning Implications: Encourages holding appreciated assets until death for tax benefits.

- Exemptions: Does not apply to assets held in certain trusts or IRAs.

However, it’s important to note that this rule primarily applies to assets that are included in the decedent’s taxable estate. Assets held in certain types of trusts, or retirement accounts like IRAs and 401(k)s, are subject to different rules and do not typically receive a step-up in basis. Therefore, comprehensive estate planning needs to consider the specific tax treatment of different asset classes.

By thoughtfully planning your estate, you can ensure your assets are passed on to your loved ones in the most tax-efficient manner possible, preserving more of your wealth for future generations. This strategic approach to estate planning is an integral part of holistic portfolio management.

Future Outlook and Potential Changes to Tax Law

While we operate under current tax laws, it is prudent for investors to consider the potential for future changes, especially as we approach 2026. Tax policy is not static; it can be influenced by economic conditions, political shifts, and societal priorities. Staying abreast of these potential changes is a critical component of proactive portfolio management, allowing you to adapt your strategies as needed.

Discussions around tax reform often include proposals to adjust capital gains tax rates, modify holding periods, or alter the step-up in basis rule. Such changes could have significant implications for investment strategies, making it essential to remain informed and flexible in your financial planning. Preparing for various scenarios can help mitigate unexpected tax liabilities.

Monitoring Legislative Developments

The political landscape plays a significant role in shaping tax policy. Major legislative changes can occur, impacting everything from individual income tax rates to corporate taxes and, crucially, capital gains. Investors should pay close attention to policy debates and proposals that could affect their investment income.

- Presidential Administrations: New administrations often bring different tax philosophies.

- Economic Conditions: Recessions or booms can prompt tax law adjustments.

- Congressional Proposals: Bills introduced in Congress can signal future changes.

- Expert Analysis: Consulting financial news and tax experts for insights.

For example, proposals to increase the capital gains tax rate for high-income earners or to eliminate the step-up in basis have been discussed in the past. While these have not yet materialized, their potential impact underscores the need for ongoing vigilance. Investors should consult with financial advisors who specialize in tax planning to understand how potential legislative changes might affect their specific circumstances.

In conclusion, while we plan based on current laws, a forward-looking perspective that anticipates potential changes is invaluable. By staying informed about legislative developments and seeking expert advice, investors can ensure their portfolio management strategies remain robust and adaptable to future tax environments.

Advanced Strategies for 2026 Tax Optimization

Beyond the fundamental strategies, advanced tax optimization techniques can further enhance your portfolio’s efficiency in 2026. These strategies often involve more complex financial instruments or sophisticated planning, requiring a deeper understanding of tax law and investment vehicles. They are particularly beneficial for high-net-worth individuals or those with intricate financial situations.

One such strategy is investing in Qualified Opportunity Funds (QOFs), which allow investors to defer and potentially reduce capital gains taxes by reinvesting them into designated low-income communities. Another involves charitable giving strategies, such as using Donor-Advised Funds (DAFs) or Charitable Remainder Trusts (CRTs), which can provide significant tax benefits while supporting philanthropic goals.

Exploring Sophisticated Investment Vehicles

Sophisticated investment vehicles offer unique opportunities for tax optimization. These options often come with specific requirements and risks, making professional guidance essential. The key is to align these vehicles with your overall financial objectives and risk tolerance.

- Qualified Opportunity Funds (QOFs): Defer and reduce capital gains by investing in specific zones.

- Donor-Advised Funds (DAFs): Contribute appreciated assets for an immediate tax deduction, then recommend grants over time.

- Charitable Remainder Trusts (CRTs): Receive income for life or a term, with remaining assets going to charity.

- Exchange-Traded Funds (ETFs) vs. Mutual Funds: ETFs often have a more tax-efficient structure due to lower capital gains distributions.

QOFs, for instance, not only provide a deferral of initial capital gains but also offer a potential step-up in basis for the QOF investment itself, and if held for ten years, the appreciation on the QOF investment can become tax-free. This makes them a powerful tool for long-term capital gains planning, especially for those with significant realized gains.

Similarly, charitable giving vehicles like DAFs and CRTs allow you to donate appreciated assets, avoid capital gains tax on the donated portion, and receive an immediate income tax deduction. These strategies not only benefit charity but also provide substantial tax advantages for the donor, integrating philanthropy with savvy tax planning.

Navigating these advanced strategies requires careful consideration and often the expertise of a financial advisor specializing in tax and estate planning. By incorporating these methods, investors can achieve a higher level of tax efficiency, preserving more of their wealth for their financial future and philanthropic endeavors.

| Key Point | Brief Description |

|---|---|

| Short vs. Long-Term Gains | Assets held over one year (long-term) receive preferential, lower tax rates compared to short-term gains. |

| Tax-Loss Harvesting | Selling losing investments to offset capital gains and up to $3,000 of ordinary income annually. |

| Tax-Advantaged Accounts | Utilizing accounts like 401(k)s, IRAs, and HSAs for tax-deferred growth or tax-free withdrawals. |

| Step-Up in Basis | Inherited assets receive an adjusted cost basis at market value on the owner’s death, reducing heir’s capital gains. |

Frequently Asked Questions About Capital Gains Tax in 2026

The main difference lies in the holding period. Short-term gains are from assets held for one year or less and are taxed at ordinary income rates. Long-term gains are from assets held over a year and benefit from lower, preferential tax rates, significantly impacting your net returns.

Tax-loss harvesting involves selling investments at a loss to offset realized capital gains. If your losses exceed your gains, you can deduct up to $3,000 against ordinary income annually, carrying forward any excess losses to future tax years, thereby reducing your overall tax liability.

Yes, the 0% long-term capital gains rate is typically available for individuals and married couples filing jointly below specific taxable income thresholds. These thresholds are adjusted annually for inflation, so it’s crucial to check the latest IRS guidelines for 2026 to determine eligibility.

The Net Investment Income Tax (NIIT) is a 3.8% tax on certain investment income, including capital gains. It primarily affects high-income individuals and couples whose modified adjusted gross income exceeds specific thresholds, adding an extra layer of taxation for affluent investors.

The step-up in basis rule allows heirs to receive inherited assets with a cost basis adjusted to the asset’s fair market value on the date of the original owner’s death. This effectively erases any capital gains that accrued during the decedent’s lifetime, reducing the heir’s potential tax liability upon selling the asset.

Conclusion

Effectively managing your investment portfolio in the context of U.S. Capital Gains Tax in 2026 is a dynamic process that requires both knowledge and proactive planning. By understanding the distinctions between short-term and long-term gains, leveraging tax-loss harvesting, utilizing tax-advantaged accounts, and incorporating smart estate planning, investors can significantly optimize their financial outcomes. Staying informed about potential legislative changes and consulting with financial professionals will be key to navigating the evolving tax landscape and ensuring your strategies remain robust and efficient. Ultimately, a well-thought-out approach to capital gains tax is not just about compliance, but about maximizing your wealth and securing your financial future.