2026 Student Loan Forgiveness: Eligibility & Benefits Compared

Anúncios

Understanding the evolving landscape of 2026 student loan forgiveness programs is crucial for borrowers seeking relief, requiring a comprehensive comparison of their unique eligibility and benefit structures.

Navigating the complex world of student loan debt can be daunting, but understanding the available relief options is a powerful first step. For those looking ahead, the year 2026 brings with it a continued evolution of programs designed to alleviate this burden. This comprehensive guide will delve into the various student loan forgiveness 2026 programs, offering a data-driven comparison of their eligibility requirements and the benefits they offer, helping you make informed decisions about your financial future.

Anúncios

Anúncios

The Shifting Sands of Student Loan Forgiveness in 2026

The landscape of student loan forgiveness is rarely static, and 2026 is expected to continue this trend with potential adjustments and refinements to existing programs. Borrowers must remain vigilant and informed about the latest policy changes and updates to effectively plan their repayment strategies. The federal government, along with various state-specific initiatives, consistently reviews and modifies these programs to address economic shifts and borrower needs.

Understanding these dynamics is vital for anyone hoping to reduce their student debt. While the core tenets of many programs may remain, specific criteria, benefit amounts, and application processes can undergo significant alterations. Staying abreast of official announcements and reliable financial guidance is paramount to capitalizing on these opportunities.

Federal Programs: A Baseline for Relief

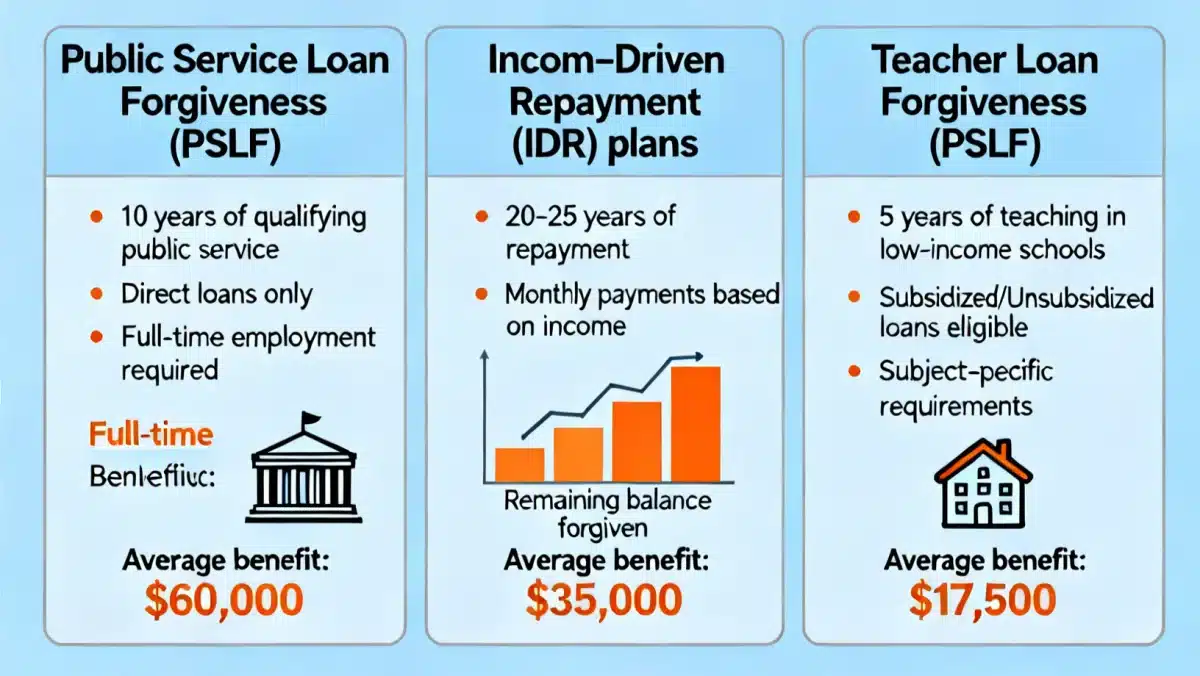

- Public Service Loan Forgiveness (PSLF): Continues to be a cornerstone for those in qualifying public service careers.

- Income-Driven Repayment (IDR) Plans: Offer pathways to forgiveness after a specified period of payments tied to income.

- Teacher Loan Forgiveness: Specifically targets educators in low-income schools, providing a direct route to reduced debt.

The collective impact of these programs on the national student debt crisis is substantial, offering lifelines to millions of Americans. However, each program comes with its own set of intricacies, demanding careful study and adherence to strict guidelines. The initial steps of identifying which program aligns with your career path and financial situation are critical for successful application and eventual forgiveness.

In conclusion, the year 2026 presents a dynamic environment for student loan forgiveness. Borrowers should anticipate ongoing changes and proactively seek out information to ensure they meet the evolving requirements of these crucial relief programs. Diligence in understanding program specifics will be key to unlocking significant financial relief.

Public Service Loan Forgiveness (PSLF): Eligibility and Evolution

Public Service Loan Forgiveness (PSLF) remains one of the most impactful federal programs for individuals dedicated to public service. In 2026, the fundamental principles of PSLF are expected to endure, requiring 120 qualifying monthly payments while working full-time for a qualifying employer. However, borrowers should be aware of potential administrative adjustments and clarity provided on what constitutes a ‘qualifying payment’ and ‘qualifying employment’ to avoid common pitfalls.

The program aims to incentivize careers in government, non-profit organizations, and other public service sectors by offering complete forgiveness of the remaining balance on Direct Loans after ten years of service. This makes it an incredibly attractive option for many, yet its historical complexity has led to confusion and denied applications. Future clarifications are always possible and necessary.

Defining Qualifying Employment for PSLF

Eligible employers for PSLF typically include government organizations at any level (federal, state, local, or tribal), and not-for-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code. Some other non-profit organizations that provide specific public services may also qualify. It is vital for borrowers to confirm their employer’s eligibility regularly, especially if they change jobs.

Full-time employment generally means working at least 30 hours per week or meeting the employer’s definition of full-time, whichever is greater. For those working multiple part-time jobs, the combined hours can sometimes count, provided each employer is qualifying. This flexibility can be crucial for individuals balancing various roles within the public sector.

- Government Entities: All federal, state, local, or tribal government organizations.

- 501(c)(3) Non-Profits: Organizations tax-exempt under this IRS code.

- Other Non-Profits: Certain non-501(c)(3) organizations providing specific public services.

The process of certifying employment annually is highly recommended to track progress and rectify any discrepancies early. This proactive approach significantly increases the chances of successful forgiveness. In 2026, the Department of Education is likely to continue emphasizing the importance of accurate and timely employment certification.

In essence, PSLF in 2026 will continue to reward dedicated public servants. Success hinges on a thorough understanding of qualifying employment and consistent tracking of payments and employment status, minimizing the risk of denial at the point of application.

Income-Driven Repayment (IDR) Plans: Paths to Forgiveness

Income-Driven Repayment (IDR) plans offer a vital safety net for borrowers whose incomes are low compared to their student loan debt. These plans cap monthly payments at an affordable percentage of discretionary income, with any remaining balance forgiven after 20 or 25 years of qualifying payments, depending on the specific plan and loan types. In 2026, IDR plans will continue to be a primary mechanism for long-term loan relief.

The federal government has several IDR plans, including Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR). Each plan has slightly different terms regarding discretionary income calculation, repayment periods, and eligibility. Borrowers should carefully compare these options to determine which best suits their financial situation and long-term goals.

Key IDR Plan Features and Forgiveness

A significant feature of IDR plans is the forgiveness component. After the designated repayment period, any remaining loan balance is typically forgiven. However, this forgiven amount may be considered taxable income by the IRS, a factor borrowers must consider. There have been ongoing discussions about potential changes to the taxability of forgiven amounts, and borrowers should monitor legislative updates for 2026.

The calculation of discretionary income is central to IDR plans. It is generally the difference between a borrower’s adjusted gross income (AGI) and 150% of the poverty guideline for their family size and state of residence. This calculation ensures that payments are genuinely affordable, adjusting as a borrower’s income or family size changes. Annual recertification of income and family size is mandatory to maintain IDR benefits.

- REPAYE: Generally 10% of discretionary income, 20 or 25 years to forgiveness.

- PAYE: Generally 10% of discretionary income, 20 years to forgiveness.

- IBR: Generally 10% or 15% of discretionary income, 20 or 25 years to forgiveness.

- ICR: The lesser of 20% of discretionary income or what you’d pay on a 12-year fixed plan, 25 years to forgiveness.

Choosing the right IDR plan and consistently recertifying are crucial steps toward achieving forgiveness. These plans provide a flexible and manageable approach to student loan repayment, ultimately leading to debt relief for those who commit to the full repayment term. Staying informed about any changes to IDR plan rules in 2026 will be essential for maximizing benefits.

In summary, IDR plans offer a structured pathway to forgiveness, aligning payments with a borrower’s financial capacity. Their continued availability in 2026 will provide significant relief, contingent upon careful plan selection and diligent annual recertification.

Teacher Loan Forgiveness: Supporting Educators in 2026

Teacher Loan Forgiveness (TLF) is a targeted program designed to encourage individuals to enter and remain in the teaching profession, particularly in underserved communities. In 2026, the program is expected to continue offering up to $17,500 in loan forgiveness for eligible teachers who complete five consecutive years of full-time teaching in low-income schools or educational service agencies. This specific benefit makes it a powerful incentive for educators facing substantial student debt.

The program specifically targets Direct Subsidized and Unsubsidized Loans, as well as Federal Stafford Loans. While not as comprehensive as PSLF, TLF provides significant upfront relief for qualifying teachers. Understanding the detailed requirements, including the definition of a ‘highly qualified teacher’ and ‘low-income school,’ is crucial for successful application.

Eligibility Criteria for Teacher Loan Forgiveness

To qualify for TLF, teachers must have taught full-time for five consecutive academic years in an eligible elementary or secondary school, or educational service agency, that serves low-income families. The school must be listed in the Annual Directory of Designated Low-Income Schools for Teacher Cancellation Benefits. Furthermore, teachers must meet the definition of a ‘highly qualified teacher’ at the time of their employment.

The amount of forgiveness depends on the subject taught. Highly qualified full-time math and science teachers at the secondary level, and highly qualified special education teachers at both elementary and secondary levels, can receive up to $17,500. Other eligible highly qualified teachers can receive up to $5,000 in forgiveness. This tiered benefit structure aims to address specific critical shortage areas within education.

- Five Consecutive Years: Full-time teaching required without breaks.

- Low-Income School: Must be listed in the official directory.

- Highly Qualified Teacher: Specific state-defined criteria must be met.

It’s important to note that borrowers cannot receive a benefit under both PSLF and TLF for the same period of service. Teachers must choose the program that offers them the most advantageous relief. Careful financial planning and understanding the long-term implications of each program are essential for educators in 2026.

Ultimately, Teacher Loan Forgiveness will continue to play a vital role in recruiting and retaining educators in critical areas. By meeting the specific eligibility criteria and understanding the benefit amounts, teachers can significantly reduce their student loan burden, allowing them to focus on their invaluable work.

State and Local Forgiveness Programs: Beyond Federal Aid

While federal programs like PSLF, IDR, and TLF form the backbone of student loan forgiveness, it’s crucial for borrowers to look beyond these options to state and local initiatives. Many states and even some municipalities offer their own loan repayment assistance programs (LRAPs) designed to address specific needs within their communities, particularly in high-demand professions or underserved areas. These programs can provide additional and often substantial relief in 2026.

These localized programs often target professions such as healthcare providers (doctors, nurses), lawyers, dentists, and other essential service workers who commit to working in specific geographic areas or with particular populations for a set period. Unlike federal programs, which can be broad, state and local programs are typically highly specialized and tailored to regional needs.

Exploring Regional Loan Repayment Assistance

The eligibility criteria for state and local LRAPs vary widely. Some programs might require a commitment of several years of service in a rural area, while others might focus on urban centers with specific shortages. Funding for these programs can come from state budgets, private foundations, or through partnerships with healthcare systems and educational institutions. It is essential for borrowers to research programs specific to their state of residence and intended profession.

Benefits from these programs can range from partial loan repayment to full forgiveness, often provided as direct payments to the loan servicer on behalf of the borrower. The application processes can also differ significantly from federal programs, sometimes requiring detailed proposals or interviews. Due to their localized nature, competition for these programs can be intense, making early application and thorough preparation key.

- Healthcare Professionals: Often targeted for service in rural or underserved areas.

- Legal Aid: Programs for lawyers working in public interest or low-income communities.

- STEM Fields: Some states offer incentives for STEM graduates to stay and work locally.

Combining state or local LRAPs with federal forgiveness programs can sometimes be possible, but borrowers must carefully review the terms of each program to avoid conflicts. It’s advisable to consult with a financial advisor specializing in student loans to navigate these complex overlapping rules effectively. The availability and specifics of these programs in 2026 will continue to be dynamic and regionally focused.

In conclusion, while federal programs are foundational, state and local forgiveness initiatives offer valuable, often specialized, pathways to debt relief. Borrowers should actively research and consider these regional opportunities in 2026, as they can significantly supplement federal aid and address specific community needs.

Navigating the Application Process and Avoiding Pitfalls

Successfully applying for student loan forgiveness in 2026 requires diligence, attention to detail, and a proactive approach. The application processes for federal and state programs, while designed to be accessible, can be complex and prone to errors if not handled carefully. Understanding common pitfalls and best practices is essential for maximizing your chances of approval and avoiding unnecessary delays or denials.

One of the most frequent issues borrowers face is incomplete or incorrect documentation. Whether it’s employment certification forms for PSLF, income recertification for IDR plans, or specific service agreements for state programs, accuracy is paramount. Submitting all required forms on time and keeping meticulous records of all correspondence and documents related to your loans is a non-negotiable best practice.

Crucial Steps for a Smooth Application

Before even beginning the application, borrowers should thoroughly review the eligibility criteria for their chosen program. This includes confirming loan types, employment dates, income thresholds, and any service commitments. Many programs have strict requirements that, if not met, will lead to automatic disqualification. A preliminary self-assessment can save significant time and effort.

Another critical step is to consolidate federal loans into a Direct Consolidation Loan if necessary. Many federal forgiveness programs, particularly PSLF, only apply to Direct Loans. Older FFEL Program loans or Perkins Loans often need to be consolidated first to become eligible. This step should be taken carefully, as consolidation can sometimes reset qualifying payment counts for some programs.

- Verify Eligibility: Double-check all criteria before applying.

- Gather Documentation: Collect all necessary forms, employment records, and income statements.

- Consolidate Loans (if needed): Ensure all loans are eligible Direct Loans.

- Track Progress: Keep detailed records of all submissions and communications.

Furthermore, regular communication with your loan servicer is vital. They can provide guidance on specific forms, confirm receipt of documents, and help clarify any ambiguities. However, it’s important to remember that servicers are primarily administrators, and while helpful, they may not always have the most up-to-date policy information. Cross-referencing information with official Department of Education resources is always a good idea.

In essence, a successful application for student loan forgiveness in 2026 is built on a foundation of careful preparation, accurate documentation, and consistent follow-up. By proactively addressing potential issues and adhering to program guidelines, borrowers can significantly improve their outcomes.

Future Outlook and Potential Changes in 2026

The future of student loan forgiveness in 2026 is subject to ongoing policy debates, economic conditions, and legislative action. While core programs are likely to remain, their specific parameters, funding, and accessibility could evolve. Borrowers should stay informed about potential reforms that might impact their eligibility or the benefits they receive, as these changes can significantly alter long-term financial planning.

One area of continuous discussion revolves around the taxability of forgiven loan amounts. Currently, under certain circumstances, forgiven debt can be considered taxable income, leading to a ‘tax bomb’ for some borrowers. There is ongoing advocacy and legislative efforts to make all federal student loan forgiveness tax-free, and borrowers should monitor any developments on this front leading into 2026.

Anticipated Policy Discussions and Reforms

Beyond tax implications, there’s always the possibility of new forgiveness initiatives or adjustments to existing ones. Policy discussions often center on expanding eligibility, simplifying application processes, or increasing benefit amounts for specific groups of borrowers, such as those with very low incomes or individuals in critical shortage professions. These potential changes could either broaden access to forgiveness or refine existing pathways.

Furthermore, the role of state and local governments in providing student loan relief is likely to grow. As federal programs face political and economic pressures, regional initiatives may become increasingly important in addressing specific community needs and providing supplementary support. This decentralized approach could offer more tailored solutions but also require borrowers to navigate a more fragmented landscape of options.

- Taxability of Forgiveness: Potential changes to make forgiven debt tax-exempt.

- Program Simplification: Efforts to streamline application and eligibility requirements.

- Expanded Eligibility: Discussions around increasing access for more borrower groups.

- Increased State/Local Role: Growth in regional loan repayment assistance programs.

Economic forecasts and inflation rates will also play a role in shaping future student loan policies. As the cost of living and education continues to rise, the pressure to provide meaningful debt relief will likely persist. Policymakers will need to balance the needs of borrowers with fiscal responsibilities, leading to continuous evolution of forgiveness programs.

In conclusion, while the core structure of student loan forgiveness programs in 2026 is likely to be familiar, borrowers must be prepared for potential shifts. Staying engaged with policy discussions, monitoring legislative updates, and understanding the evolving economic context will be crucial for navigating their student loan journey effectively.

| Key Program | Brief Description of Benefits |

|---|---|

| PSLF | Forgiveness of remaining Direct Loan balance after 120 qualifying payments in public service. |

| IDR Plans | Payments capped at discretionary income, forgiveness after 20-25 years. |

| Teacher Loan Forgiveness | Up to $17,500 for qualifying teachers in low-income schools after 5 years. |

| State/Local LRAPs | Varied repayment assistance for specific professions or service in critical areas. |

Frequently Asked Questions About 2026 Student Loan Forgiveness

The primary federal programs expected in 2026 include Public Service Loan Forgiveness (PSLF), various Income-Driven Repayment (IDR) plans leading to forgiveness, and Teacher Loan Forgiveness. Each has distinct eligibility criteria and benefits designed for different borrower circumstances and career paths.

To determine if your employer qualifies for PSLF, they must be a government organization (federal, state, local, or tribal) or a 501(c)(3) non-profit. You should submit an Employment Certification Form annually to the Department of Education to confirm eligibility and track your progress.

The taxability of forgiven student loan amounts can vary. While some federal forgiveness (like PSLF) is non-taxable, others, particularly under IDR plans, might be considered taxable income by the IRS. It’s crucial to consult with a tax professional and monitor legislative updates for 2026.

Yes, in addition to the federal Teacher Loan Forgiveness program, many states and local municipalities offer their own loan repayment assistance programs (LRAPs) for educators. These often target specific subject areas or underserved school districts, providing additional pathways to debt relief.

Begin by verifying your eligibility for specific programs, gathering all necessary documentation, and ensuring your loans are eligible (consolidate if needed). Maintain meticulous records and communicate regularly with your loan servicer. Proactive annual certification is key to a successful application process.

Conclusion

As we look towards 2026, the landscape of student loan forgiveness remains a critical area of focus for millions of Americans. The federal programs, including PSLF, IDR plans, and Teacher Loan Forgiveness, continue to offer substantial pathways to debt relief, each with distinct requirements and benefits. Supplementing these federal initiatives are various state and local programs, providing tailored assistance for specific professions and communities. Successfully navigating these options demands a proactive approach, meticulous record-keeping, and a thorough understanding of eligibility criteria. By staying informed about potential policy changes and diligently managing the application process, borrowers can significantly alleviate their student loan burden, paving the way for a more secure financial future.